One of the most frequent questions asked nowadays is, “Has the market bottomed or will it go lower?”.

This comes after global indices fell on average by 30% in March, only to recover more than half of that fall by mid-April. This has left many unsure as to the direction of the next move, and investors are more confused than ever when the market rebound comes amid recent disastrous macroeconomic data.

How to View Market Direction

Many investors think that their investment decision needs to be an all-or-nothing strategy. For example, if they think that the market is going up, they feel they should put 100% of their investments into the market. Likewise, if they think the market is going down, they will stand aside without investing in anything and wait for what they deem to be “the bottom” before going in.

Unfortunately, this is akin to timing the market, which is already quite a difficult skill to get right under normal market conditions – and made almost impossible in today’s uncertain and volatile market.

For us, we prefer to think of a market’s direction in terms of probabilities. For example, at this point, we believe that there is a higher risk to the downside for markets – so we attach a 70% probability to it, and assign a 30% probability of it going up.

Our Preferred Investment Strategy

We believe that there is a particular strategy which suits the current situation very well: “dollar cost averaging”, commonly known as “DCA”. The DCA strategy merely means one should break up one’s intended investment amount into several instalments – in other words, make a series of periodic bite-sized investments over a period of time instead of a single lump-sum investment. For instance, someone who has $10,000 can choose to invest $1,000 into the market every month over 10 months or $500 a month over a 20-month period.

In order to explain why we have chosen DCA as our preferred strategy, let’s take a hypothetical example where Mr A has $18,000 to invest. Assuming he adopts an 18-month DCA. This works out to investing $1,000 per month over a period of 18 months.

In the case where we are right and the market does go down from here, what the DCA will do is buy into the market at lower and lower prices. This helps to bring down the average buy-in price. The idea is to get an average buy-in price that is as close as possible to the bottom. Notably, this strategy can never “pick the bottom” because the DCA strategy is an average price of numerous prices across a period of time and not a single buy-in price. In other words, this strategy acknowledges the fact that no one knows where the exact bottom will be for the market.

But what happens if the market surprises and goes higher instead? In this case, the DCA strategy will be buying into a higher and higher price but at an average price which trails the actual market price. This ensures that the investor is not left behind by an unexpected rally.

How Long Should the DCA be?

While there is no so-called right or wrong answer for this, we believe that a slightly longer DCA of say 18-24 months is preferable in the current market. Judging from what we have seen in the past two crisis of 2000 and 2008, DCAs of between 18 and 24 months have worked particularly well.

We also like longer-duration DCAs because of the flexibility it provides. What we mean by this is that investors who take up a short-duration DCA (of say 6 to 12 months) would end up committing all their capital within a short space of time.

The risk is that, if the downturn turns out to be nastier than expected, like in the case of the Great Depression of 1929, investors will be stuck with a high buy-in price. However, for those adopting an 18-month DCA, they have the flexibility – say after 10 months – to suspend their remaining 8 instalments should things turn much worse. These remaining 8 instalments could, for example, be stretched to a further 16 months by adopting a DAC of 1 instalment every other month instead.

DCA in Action

Let’s take a look at how 3 different strategies would have worked out during the previous two major crashes we have experienced over the past 20 years, namely: The Global Financial Crisis of 2008 and The Dot Com bust of 2000. The 3 strategies that we will be comparing are the lump-sum, 6-month DCA and 18-month DCA.

-

2008 Global Financial Crisis (V-shaped recovery)

In this example, we assume that an investor adopts all the above-mentioned strategies in May 2008 (closing price = 1400) just as the market pulled higher after an initial sharp sell-off. The results are as follows:

Strategy Average Buy-in Price Number of Months to Break-Even Lump-Sum 1400 47 Months 6-Month DCA 1227 27 Months 18-Month DCA 1019 -2 Months What is interesting is that the 18-months DCA strategy continued through the bottom of the crisis and into the early part of the recovery. At the point, the 18-month DCA was completed and the average buy-in price was established to be 1019, the market was at 1036 – which means that the strategy had broken-even 2 months prior and was already “in-the-money” when the DCA was completed.

Chart 1: S&P 500 during The Global Financial Crisis

Source: FA Wealth Management Department

-

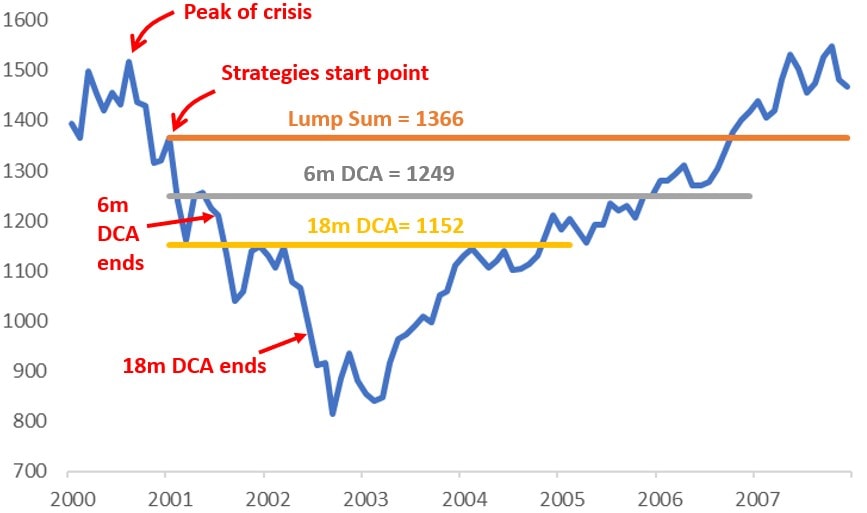

2000 Dot Com Bubble Bust (U-shaped recovery)

In this example, we assume that an investor adopts all the above-mentioned strategies in January 2001 (closing price = 1366) just as the market pulls higher after an initial sharp sell-off. The results are as follows:

Strategy Average Buy-in Price Number of Months to Break-Even Lump-Sum 1400 47 Months 6-Month DCA 1227 27 Months 18-Month DCA 1019 -2 Months What is interesting is that this decline was more of a U-shaped recovery, which means it took longer to reach the bottom and when it did, took longer to recover compared to a V-shaped recovery. As such, even the 18-months DCA strategy was left with an average buy-in price that took 29 months to break even. Nevertheless, when compared with the other two strategies, this remains the far more superior one.

Chart 2: S&P 500 during The Dot Com Bubble Bust

Source: FA Wealth Management Department

Conclusion

In summary, many investors understandably remain uncertain and apprehensive. However, history has proven that, by using both the concept of time and the correct strategy, investors can significantly increase the odds of making this a profitable journey. For us, this is reflected in our Market Recovery Portfolio, which uses an 18-month DCA Strategy. We believe this will be well worth considering amid this current crisis.