Contributed by Poh Liang Siah,Financial Advisory Manager, Financial Alliance Pte Ltd

(The contributor can be contacted at liangsiah@fapl.sg)

Author’s Disclaimer: My comments are based on my recent personal experience of being an executor for a deceased family member and solely represent my own views.

Unbeknown to me, I was named an executor in a will of my family member. When the testator passed on, I was kicked into action. Here are some three things I learnt from my experience which may help you to decide if you should take up the role should anyone ask of you.

1. Personal Time Required

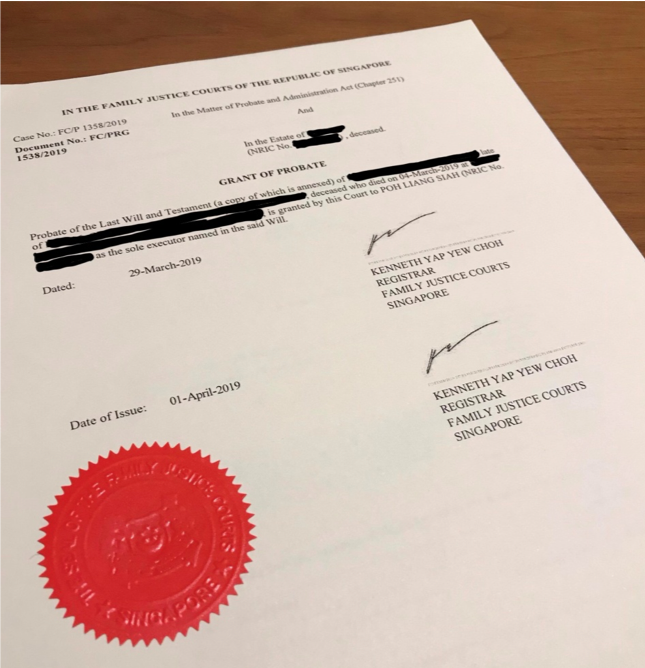

Thankfully mine was a straightforward case with a will in place. It only took 13 days for the Family Justice Court to issue the Grant of Probate (I was assisted professionally by our business partner from Falco Heritage to apply for the Grant of Probate).

Still, it took 2 trips to the Family Court, one trip to Commissioner for Oaths’ office to get the Grant of Probate. Thereafter it was one trip to the bank for account closure. Do expect more trips if you have more legal documents to submit and accounts with other banks to close.

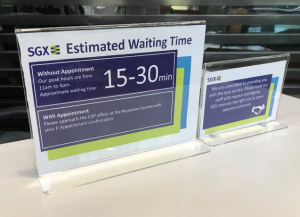

Then there was a visit to The Central Depository (“CDP”) at Buona Vista (thankfully not too far flung) to convert the deceased’s CDP account to an estate account. The average waiting time there stated in bold on a prominent signboard was 15 to 30 minutes.

If you have not done up your will, do get it done soon so that your family will not be put through a more costly and lengthier process to get a Letter of Administration! In other words, with a will, as it is in my case, the court will issue a Grant of Probate, but without a will, the court will issue a Letter of Administration instead (which takes longer than issuing a Grant of Probate), and the deceased’s estate will be stuck in limbo for a longer time.

And do consider asking the person you have in mind to be the executor if he or she will be willing to do it. If the intended executor declines the role, wouldn’t it be better if the testator finds a replacement before passing on? Out of goodwill or gratitude, do consider apportioning a small token for your executor for sacrificing his time to administer your estate — your lawyer may not suggest that to you.

2. Extended Management of Estate Assets

The deceased left behind a list of assets, and that was truly helpful in my case. I could dispense with the need to visit all the banks and insurance companies to gather all policy and bank account information.

Do note that, for insurance policy claims, the insurer may ask for an Attending Physician’s Statement when the cause of death is an illness, or when other circumstances relating to the claim require them to do so. Insurers may use that Statement for purposes such as to rule out non-disclosure of pre-existing conditions during insurance application, which may void the contract altogether. In my case, I was able to get the insurers to waive the Attending Physician Statement based on the facts leading to the death and the policy type, saving the deceased’s family a few hundred dollars of report fees they would otherwise incur.

If the deceased had held shares — here’s where it gets interesting — every transaction to sell shares has to be submitted by the executor in person over the counter at the CDP. No online submission is allowed! Should the beneficiaries choose to dispose of the shares in a piecemeal manner over an extended period of time, that means more trips to the CDP and the bank.

To receive the proceeds from CDP, an estate bank account in the deceased’s name needs to be opened. All transactions are to be done by the executor in person at the banks. Again, no internet banking facilities can be used!

As it turned out in my case, the estate’s CDP account has a stock that was suspended from trading, so I can’t do anything to close off the account and fully discharge my duties just yet. Also, should I pass on tomorrow, the executor of my estate will take over my unfinished executor duties!

3. Possible conflict with Beneficiaries

The selfish way is for me to sell off everything or transfer the shareholdings to the beneficiaries and leave them to decide what to do from there. That would give me the least hassle.

However, since we all have different ideas as to what is a good stock to continue holding and when is a good time to sell, you might get negatively implicated if you influenced the decision and it turns out less than ideal. You can imagine the potential friction you will have with beneficiaries who are less knowledgeable and less competent to make such decisions, but still want to partake in the decision. It gets worse when you add differences in personalities to the equation. The bottom line is, we have to act tactfully and sensibly here.

Conclusion & Reflections

If you already feel daunted by the process I have gone through for a simple case, then perhaps being an executor is not for you. It would be worse if your work demands a lot of your presence.

Although there were inconveniences I had to go through, yet as a final service to the deceased, I gladly did it. We should sincerely render help to the family should our personal capacity allow it. We go through the trouble for the family so they can better focus on getting back on their feet.